Seller Financing: Is It Right For Me?

In this high interest rate environment, it can make sense for both buyer and seller to consider seller financing, as it can be quite lucrative for the seller and solve down payment or credit challenges for the buyer.

For a Buyer, paying a 5% interest rate is almost always preferable to an 8% interest rate. For certain sellers, collecting $1M today vs $1M in 5 years plus $50k per year may be quite attractive.

Here’s an overview of Seller Financing and a few SF properties that are for sale right now offering better-than-market rates.

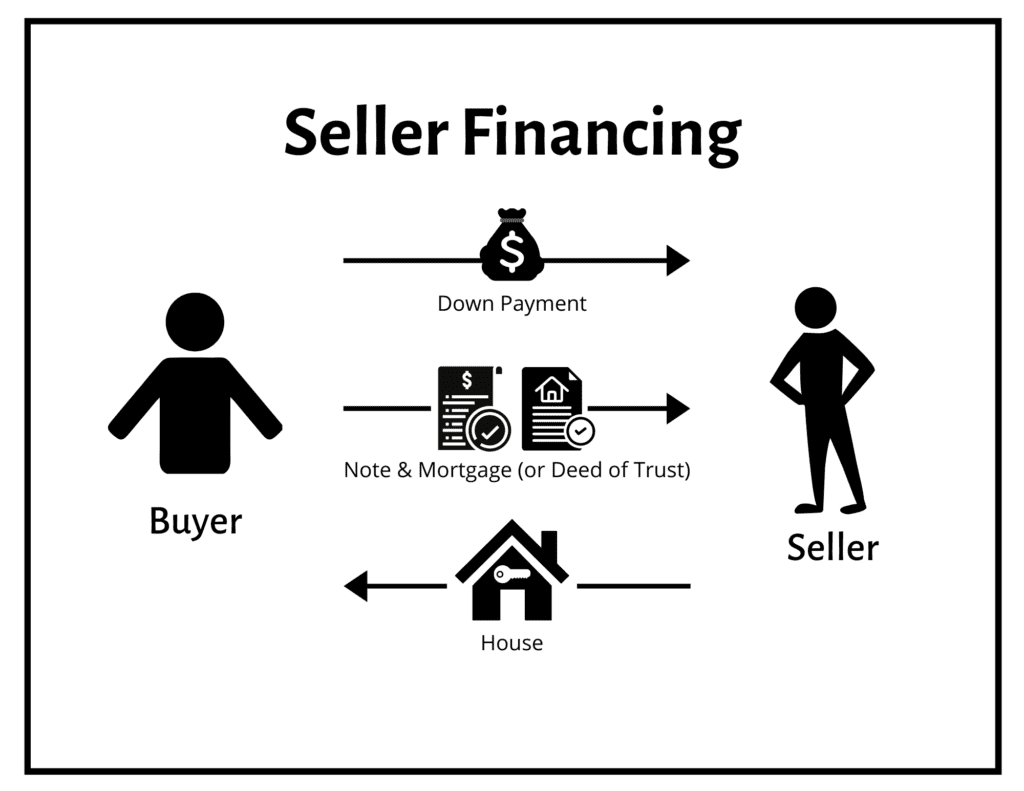

WHAT IS SELLER FINANCING?

Seller financing is where the seller takes the role of a lender and the buyer agrees to pay the seller back overtime with interest in exchange for collateral of the property. If the buyer defaults on the loan, the seller can foreclose and take the property back.

If you’re considering seller financing, your agent can help you negotiate the terms, but you should really have a lawyer review everything to make sure you understand everything before signing anything.

HOW DOES IT WORK?

In exchange for the title to the property the buyer agrees to pay the seller back over time, with interest and a down payment. The seller records a lien or deed of trust on the property just like a traditional lender would. At that point the Seller becomes the lender and is no longer on title or responsible for maintenance, taxes, insurance or anything else related to the property.

The buyer then pays the seller according to the terms of the note. It can really be just about anything the two parties agree as long as it doesn’t run afoul of predatory type practices like payday loans in California for example.

Seller financing first and foremost requires the seller to have 100% equity or at least a very low balance on their mortgage relative to the sale price. If the seller has a loan, their lender will in most cases require their loan to be paid off at the time of sale, so that money has to come from somewhere, which is where the down payment comes in.

If the buyer’s down payment doesn’t cover the sellers loan balance, the seller needs to find that money from somewhere else. There may be some situations where an assumable loan could possibly work, but that’s for another video.

Some things to consider, as this is not a very regulated process so it’s important that the buyer and seller understand they are entering into a lending relationship of some period of time and that comes with risks and rewards.

$749k | 3BD, 1bA | 1,020 sqft

Rare Floating Home in Mission Bay on Mission Creek

Seller Financing at 6% for 5 years with 30% down

Save $772/mo vs 7.55% at today’s average rate (10-Nov, 2023)

Listing courtesty of Generation Real Estate, Danny Yadegar

WHAT ARE THE BENEFITS?

For sellers, you’re able to collect interest on the money that the buyer owes you. That rate is determined by mutual agreement from both parties during negotiations. Since rates right now are averaging 7.55% (per Mortgage News Daily, 10-Nov, 2023), you can give the buyer a deal by offering them a point or two less than current rates and make some passive income over time. A $1M loan at 5% is $50 thousand dollars per year - and you don’t have to do a whole lot other than cash the checks.

If the buyer is riskier and a traditional lender may not take them on, you could charge more than the going rate - perhaps 10% or 12%, which is comparable to a hard money lender, but that comes with a higher risk of default. If the banks won’t lend to them, and if banking or risk management is not your primary business, you should think long and hard if you’re really wanting to get into bed with that buyer.

$1.329M | 2BD, 1BA | 1,050 sqft

Fully Detached Single Family Home in Bernal Heights

Seller Financing at 5.5% - 6% with 25% - 30% down

Save $1,344/mo w/25% down at 5.5% vs 7.55% at today’s average rate (10-Nov, 2023)

Listing courtesy of Coldwell Banker, Paige Geinger

WHAT’S THE EXIT STRATEGY?

At the end of the term, the duration of which is also fully negotiable, the buyer pays the seller back the balance of the amount owed. They usually get that money from refinancing or from selling the property. A common loan period we see is 5 years.

Both the buyer and the seller need to fully understand and be able to articulate the buyer’s exit strategy. If the buyer is flipping the property, do they have the cash to do the work properly so they’ll have the equity to pay you back? If they’re W2 employees or self-employed, do they have a stable job and income history such that they’ll be able to get a loan when the term comes up?

$798,950 | 1BD, 1BA | 657 sqft

Newer Constructed View Condo in Hunters Point

Seller Financing at 3% with 20% down

Save $1,796/mo w/20% down at 3% vs 7.55% at today’s average rate (10-Nov, 2023)

Listing courtesy of eXp of California, Brendon Yim and Brian Cen

WHAT ARE THE RISKS?

The biggest risk is of course default. Even with the best of intentions, sometimes folks can get over their skies and can’t pay back their obligations. As the lender, you now have to decide how to make something work. Your ultimate backstop is foreclosure and that’s a process that you should definitely not try to take on yourself unless that’s your business. But there may be other options in between depending on the unique situation of the buyer.

If you foreclose, the buyer loses the property plus their down payment and any principle they’ve paid down, which is why more down payment is better. That’s their skin in the game. A buyer that’s in a bad spot will likely behave very differently if they have five HUNDRED thousand dollars to lose, vs five thousand or nothing.

And once you complete the time consuming and stressful foreclosure process, now you have the house back to sell again. Hopefully it’s in the same or better shape then when you sold it but there are no guarantees. If it’s a flip that got stopped mid way, you could be sitting on a real disaster.

$1.995M | 4BD, 4BA | 2,185 sqft

Stunning Crocker Amazon Single Family Home

Seller Financing at 6.5% with 30% down

Save $986/mo w/30% down at 6% vs 7.55% at today’s average rate (10-Nov, 2023)

Listing courtesy of Engel & Volkers, Eric Rahe

IS SELLER FINANCING FOR ME?

Seller financing is not for everyone but it can create a very helpful path forward for both parties where one might not have existed otherwise. Please consult an attorney before signing anything. We know some excellent attorneys that specialize in this in the Bay Area and can help.

If you’re thinking of buying, selling or investing in real estate, whether you’re paying cash or getting a loan or even want to talk about seller financing in more detail, give us a call. We’re happy to help.

Note: rates and calculations are provided in this email for educational purposes only and provided as examples of what may be possible. These are not quotes and can/will change. Rates fluctuate on a daily/hourly basis as well as based on the strengths of the borrower and particulars about the property. If you need a mortage broker, I’m happy to refer you to some excellent professionals.